- The traditional separation of growth and value investing can be misleading

- Benchmark construction often has meaningful overlap between growth and value

- Robeco BP Global Premium Equities’ approach goes beyond style classifications

Investing in value equities, especially those outside of the US, has grown in favor as a means of diversifying away from the US market dominated by Big Tech, and growth investing itself. With concentration risk beginning to fuel negative investor sentiment toward many of the Magnificent Seven and other AI-related businesses, investor appetite has shifted, now favoring mispriced businesses exhibiting similar quality and earnings momentum characteristics.

The Robeco BP Global Premium Equities strategy offers such a channel, but how the value style is defined has been the subject of debate. In its new white paper, ‘Redefining value: From style category to investment discipline’, Boston Partners offers its perspective into how investors should be wary of viewing value and growth as polar opposites, when in fact there is considerable overlap and fluidity in both styles.

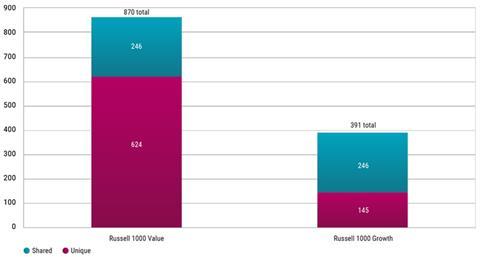

This can be seen in benchmarks such as the Russell 1000 Value Index and the Russell 1000 Growth Index, which are widely used to represent the two style universes and are often seen as rivals, despite having nearly 250 stocks in common. Many are members of both indices, as can be seen in the chart drawn from the white paper below, blurring the lines between growth and value investing.

Past performance is no guarantee of future results. The value of your investments may fluctuate. Source: FTSE Russell; Boston Partners, February 2026.

There are also contradictions in the constituent members. Big Tech firms are often labeled as growth stocks by default, even though they have profitability profiles, free cash flow generation and capital return policies resembling traits historically associated with value. Conversely, Consumer Staples companies, which are seen as archetypal value stocks, often have higher earnings growth potential and pricing power more typically linked to growth stocks.

These indistinctions can present problems for an institutional investor tasked with allocating to one style or the other. Would a mandate be breached if a company drifted from one style to the other, or appeared in both? Economic and market conditions constantly change, so it is useful to look outside this spectrum and use more definitive criteria.

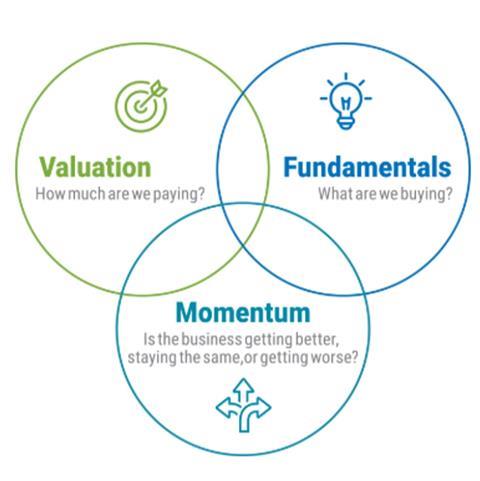

The white paper outlines how Boston Partners has remained highly disciplined in their search for value equities, never deviating from their time-tested ‘Three Circles’ approach. For them, the valuation factor – the price at which a company is trading, and whether it reflects the real underlying potential of the business – is only one aspect to consider. Using this factor solely runs the risk of meeting the value trap, where a company is cheap for a reason.

Rather, it is important to consider two other factors within the mix: business fundamentals that are durable, and improving momentum, where its earnings outlook is improving, rather than getting worse.

For Boston Partners and its Global Premium Equities strategy, valuation is foundational, but never isolated; the real value of a business cannot be defined by static multiples alone. Great attention is paid to metrics such as price to cash flow, return on invested capital (ROIC), operating return on operating assets (OROA) and, importantly, improving earnings momentum.

Finding mispricings

The goal is not to optimize for any single statistic, but to identify situations where valuation does not fully reflect operational strength and long-term compounding potential. The portfolio managers at Boston Partners often find that mispricings reside in the gap between perception and underlying business reality. This can produce genuine upside when the market revalues the stock when its potential becomes clearer.

This approach is also useful for watching for when a company displays two of the three circles. Each Boston Partners analyst maintains a watch list of companies which could, for example, have compelling fundamentals and positive momentum but don’t yet meet the valuation criteria. During periods of market stress or style rotation, valuation gaps can close rapidly. When they do, two-circle stocks can transition into actionable three-circle investments.

A disciplined framework

The white paper concludes that true value across market cycles is more likely when a business demonstrates fundamental resilience, trades at a reasonable valuation relative to its prospects, and exhibits improving earnings and profitability characteristics. Together, they form a disciplined framework for underwriting change beyond the style box and for compounding capital as businesses evolve.

For more information, please see our dedicated web page explaining how the Global Premium Equities strategy, value investing, and the rest of the Robeco Boston Partners range can work for you. Find out more at the link below.

Important information.

Marketing communication for professional investors only. Capital at risk. This information refers only to general information about Robeco Holding B.V. and/or its related, affiliated and subsidiary companies, (“Robeco”), Robeco’s approach, strategies and capabilities. This is a marketing communication intended solely for professional investors, defined as investors qualifying as professional clients, who have requested to be treated as professional clients or who are authorized to receive such information under any applicable laws. Unless otherwise stated, the data and information reported is sourced from Robeco, is, to the best knowledge of Robeco, accurate at the time of publication and comes without any warranties of any kind. Any opinion expressed is solely Robeco’s opinion, it is not a factual statement, and is subject to change, and in no way constitutes investment advice. This document is intended only to provide an overview of Robeco’s approach and strategies. It is not a substitute for a prospectus or any other legal document concerning any specific financial instrument. The data, information, and opinions contained herein do not constitute and, under no circumstances, may be construed as an offer or an invitation or a recommendation to make investments or divestments or a solicitation to buy, sell, or subscribe for financial instruments or as financial, legal, tax, or investment research advice or as an invitation or to make any other use of it. All rights relating to the information in this document are and will remain the property of Robeco. This material may not be copied or used with the public. No part of this document may be reproduced, or published in any form or by any means without Robeco’s prior written permission. Robeco Institutional Asset Management B.V. has a license as manager of UCITS and AIFs of the Netherlands Authority for the Financial Markets in Amsterdam.