During the past quarter century or so, a blend of European credit would have delivered better returns at lower risk than the standard balanced portfolio

Investors can’t afford to ignore credit, especially European investors.

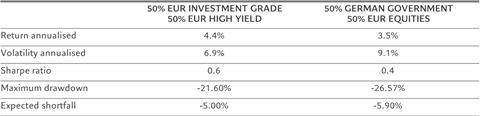

We find that a balanced mix of euro investment grade credit and euro high yield credit would have outperformed an equally balanced allocation split between German government bonds and European equities over the period since a European high yield index was first launched in 2001. What’s more, the credit portfolio’s return and risk profile has been better in both rising and falling interest rate environments.

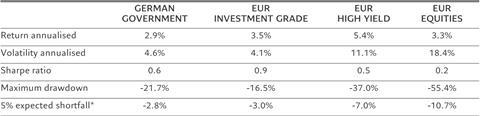

Overall, credit offers better Sharpe ratios – the balance between risk and return – than the more traditional asset classes. So, for instance, euro investment grade credit has offered better returns at lower volatility than German government bonds – the standard “risk-free” instrument. And high yield credit has generated considerably better returns for substantially lower risk than European equities. At the same time, investment grade and high yield credit have had substantially lower maximum drawdowns than German government bonds and European equities respectively (see Fig. 1), while corporate failure is more catastrophic to equity investors than to corporate bond holders.

Figure 1 - Performing credit Asset class summary 2001-23

*Average return of the 5% worst months over the 2001-2023 period. Source: Pictet Asset Management Developed Markets Credit, ICE BofA, Bloomberg. Data covering period 31.01.2001 and 30.11.2023.

And unlike investing in equity where market timing can make a very significant difference in long-run returns, the fact that bonds come with fixed maturities makes market timing less important. Economic growth matters less to holders of corporate debt than it does to owners of equity. And while credit is often seen as a hybrid asset class, showing both bond- and equity-like characteristics, that’s also true of equities, especially in some sectors.

In a nutshell, investors need to re-think the role of credit in their portfolios. Credit should be core.

02 Demystifying credit

When investors think of credit, they tend to focus on risk. Investment grade credit is seen in light of corporate uncertainty while government debt represents safety. High yield is often associated with default risk whereas equities represent opportunities such as growth and value. To be sure, investors ought to balance opportunities and risks. The evidence shows that credit offers a better risk-reward profile than corresponding equities and government bonds.

History shows investing in credit delivers steady returns. The asset class’s drawdowns have been temporary, and have always been followed by strong performance rebounds, rewarding the patient investor.

Since 2001 (when data was first available) European investment grade has generated superior returns to German bunds for a similar level of annual volatility, resulting in a significantly better Sharpe ratio.

Over the same period, European high yield credit has generated better returns at lower volatility than European equities, which have failed to compensate investors for the very high level of risk taken, resulting in a poor Sharpe ratio, and have been exposed to extreme negative returns, as shown by the maximum drawdown and expected shortfall.

As a result, replacing German government bonds with European investment grade credit and European equities with European high yield credit delivers 0.77 percentage points more in annual return, with significantly less volatility and less drawdown. At the same time, the credit portfolio posts smaller average losses during the worst market downturns (see Fig. 2).

Figure 2 - A fine balance Asset class combinations, 2001-23

Source: Pictet Asset Management Developed Markets Credit, ICE BofA, Bloomberg. Data covering period 31.01.2001 and 30.11.2023.

This result remains the same whether central banks are raising interest rates or cutting them (see Figs. 3 and 4). Setting the 10-year German sovereign rate as the reference rate, the properties of the two portfolios have been computed during the years when the interest rate has been increasing (10 years out of 23) and during the years when the interest rate has been decreasing (13 years out of 23). In both environments, the credit portfolio exhibits superior returns with lower volatility, and therefore a better Sharpe ratio, in comparison to the mix of government debt and equities.

Figure 3 - When rates go up… Blended portfolio performance in rising rate years

Pictet Asset Management Developed Markets Credit, ICE BofA, Bloomberg. Data covering period 31.01.2001 and 30.11.2023.

Figure 4 - …and when they fall Blended portfolio performance in declining rate years

Pictet Asset Management Developed Markets Credit, ICE BofA, Bloomberg. Data covering period 31.01.2001 and 30.11.2023.

When faced with interest rate and growth risk, investors also often downplay credit as a hybrid asset class relative to “pure” equities and government bonds. That’s a mistake. In reality, all of these asset classes incorporate opportunities and threats that are related to interest rates and systemic risks. Credit, however, offers better risk-adjusted returns and stronger recover rates after temporary downturns.

03 Credit at the heart of an optimal portfolio

A portfolio optimisation analysis presents a similar picture.

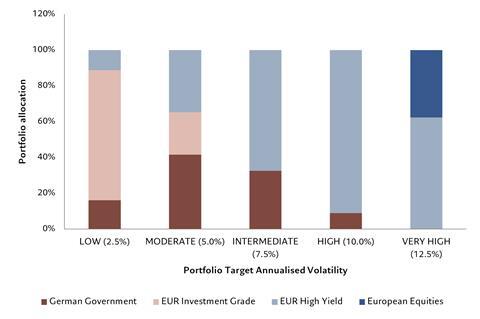

Whatever an investor’s risk tolerance, a portfolio of government debt and equity never produces the optimal portfolio when credit is also an alternative (see Fig. 5). We find that for each targeted level of risk, adding credit to an allocation produces a more optimal portfolio.

For a low-risk portfolio, the optimal allocation is essentially investment grade credit, with a small allocations to sovereign debt and high yield for the benefits of diversification.

Figure 5 - Credit, whatever the risk preference Optimal risk-adjusted portfolio allocation by the level of risk, 2001-23

Source: Pictet Asset Management Developed Markets Credit, ICE BofA, Bloomberg. Data covering period 31.01.2001 and 30.11.2023.

For a moderate risk profile, we obtain more balance between sovereign debt, investment grade and high yield credit.

For riskier portfolios (intermediate and high level of volatility), the high yield asset class dominates the portfolio, with some sovereign debt to bring in diversification.

Finally, for a very high level of volatility, equities comes into the mix.

04 Opportunities outweigh risks

Investors tend to overlook the richness of the asset class – the variety of issuers and instruments has expanded greatly in recent years. In Europe, particularly in investment grade credit, the market has broadened and matured appreciably over the past few decades.

At the same time investors are overly pessimistic about default rates on high yield bonds.

The fact is that investors are more than compensated against the risk of default with credit spreads – the amount of additional premium they generate over risk-free interest rates – for the default risk they bear.

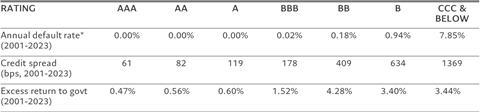

As the data show (see Fig. 5), the annual face value lost on defaults over the entire European credit universe (investment grade and high yield) has averaged 0.09 per cent over the past two decades. An investment grade credit investor is nearly always repaid the face value of the bond on maturity, along with regular interest payments. In light of this, there’s no objective reason to buy government debt instead, since investment grade credit delivers more return for a similar level of risk.

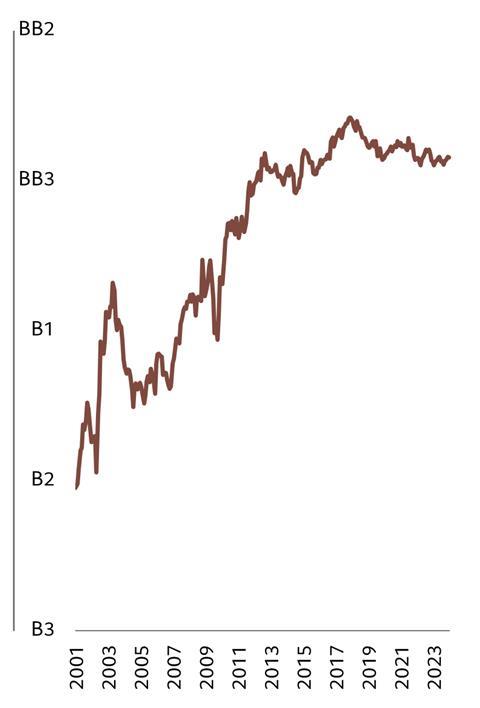

Figure 6 - To BB or not to BB Average annual default rate by rating, Europe

*Face value weighted bond default rate from ICE European High Yield Index. Source: Pictet Asset Management Developed Markets Credit, ICE BofA, Bloomberg. Data covering period 31.01.2001 and 30.11.2023.

The average annual default for investment grade issues – those rated BB or higher – is negligible. Default risk only becomes relevant for credits rated B and only becomes significant for those rated CCC and below. But at the same time, the premium investors receive for bearing credit risk rises rapidly the lower the credit rating. In fact, credit spreads more than compensate investors across the rating spectrum, since the average annual excess return, including loss on defaults, remains positive for all credit ratings.

Figure 7 - Quality improvement European high yield index average rating, 2001-23

Source: Pictet Asset Management Developed Markets Credit, ICE BofA, Bloomberg. Data covering period 31.01.2001 and 30.11.2023.

To put this into perspective, it’s important to remember that when companies go bankrupt, their equity is often wiped out. For example, between 1980 and 2019 more than 400 companies were removed from the S&P 500 because after not recovering from distressed levels. This corresponds to an annual average of 2 per cent of companies in the index. By contrast, the average annual default rate for European high yield issues is 1.3 per cent of index face value since 2001. What’s more, when companies go bust, the value of their equity goes to zero, leaving investors with little. By contrast, investors have, on average, seen a recovery rate of 40 per cent on high yield credits in default over the past 20 years. Nor does this consider that active investment teams can help companies avoid default.

At the same time, the credit quality of European high yield issuers has improved noticeably over the last two decades, rising two notches from B2 to BB3. This is significant: the estimated historical average probability of default of the BB3 rating category is 0.37 per cent, well below B2’s 0.94 per cent. In other words, investors in European high yield credit are less exposed to default risk than in the past.

05 Shock absorbing

Credit pays an income and its price steadily converges to its face value as the bond approaches maturity.

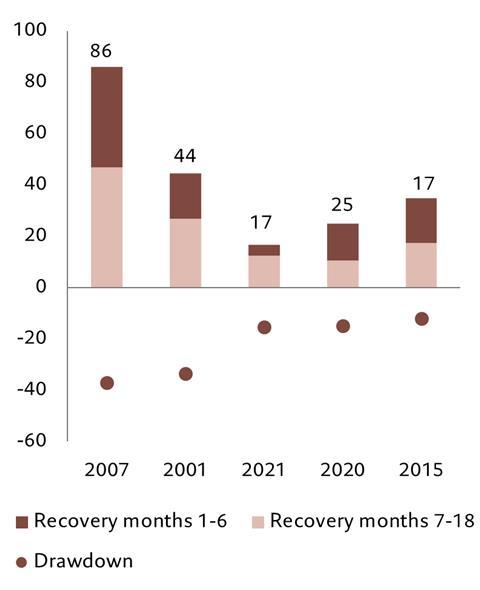

Figure 8 - Bouncing back… European high yield 18 months return following a drawdown, 2001-23

Source: Pictet Asset Management Developed Markets Credit, ICE BofA, Bloomberg. Data covering period 31.01.2001 and 30.11.2023.

As a result, market shocks that cause the bonds to drop in value are time limited – once the shock passes, credit tends to stage a strong recovery. By contrast, equity losses can persist after serious market dislocations. That’s because credit offers contractual returns, unlike equities.

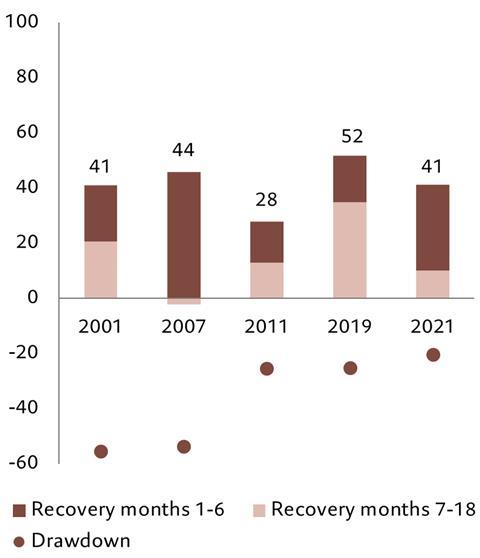

Historically, recovery in European high yield is always well under way within six months of a market drawdown of at least 10 per cent and occasionally has posted a full recovery. And in all cases losses have been erased by 18 months following the market drop. Similar results also follow less severe drawdowns. By contrast, European equities have tended to have much slower and less complete recoveries after severe drawdowns.

Trying to time the market makes little sense – few can do so accurately – and missing entry points represents huge opportunity costs.

Figure 9 - …faster than equities European equities 18 month return following a drawdown, 2001-23

Source: Pictet Asset Management Developed Markets Credit, ICE BofA, Bloomberg. Data from 31.01.2001 to 30.11.2023.

Strategic allocation and patience reward the long-term investor in credit: the pull-to-par drives the bond price higher, and the carry is realised. Chasing optimal exit and entry points in credit – in other words, trying to time the market – can come with a considerable opportunity cost, especially since credit recoveries tend to be swifter than that for equities.

And that’s without taking into account the additional benefits that credit offers. Such as that companies tend to issue new bonds at a discount, giving those early investors a built-in return. Or the liquidity premium attached to small bond issues. Or the fact that investors can improve the return their credit portfolio generates by allocating along the yield curve – longer dated bonds tend to generate higher yields. Or that credit often comes with optionality, a complexity that can lead to mispricing and therefore investment opportunities for those who have the tools to analyse the bonds.

06 What matters to credit

Credit markets are most sensitive to shocks in refinancing costs, which, in turn, are primarily determined by shifts in monetary and fiscal policy. Monetary policy is driven by a combination of real growth, inflation and excess leverage risk, with the latter two the biggest factors in changes to the risk-free rate and hence refinancing risk. By contrast, real growth rates tend to move within a narrow range and never shift suddenly.

Over the past fifty years, credit has steadily delivered stronger returns than government debt, across most growth and inflation regimes. Low growth environments have tended to be very favourable to credit, to the detriment of equities. On the other hand, while credit suffers during periods of high inflation, so to do equities.

“Investors who patiently apply longer investment horizons to credit allocation are rewarded.”

Credit is no more a hybrid asset class than are equities. And timing the credit market is much less relevant than it is to equity investors, where missing an entry point can make a very substantial difference to returns. Instead, investors who patiently apply longer investment horizons to credit allocation are rewarded.

Finally, the credit asset class offers additional opportunities beyond collecting the yield, that investors can harvest. We have designed our investment process with these all of these factors in mind to maximise the prospect of generating positive and steady excess returns over the long run.

Websites

We are not responsible for the content of external sites

We believe Europe is entering a transformative period of economic renewal driven by reforms, public investment and a focus on sustainability and digital innovation. These developments are expected to drive long-term growth and create a more resilient and competitive economic landscape, creating opportunities for investors at a time when the US is facing mounting challenges.

Pictet has been building active thematic strategies since the 1990s. Our Global Thematic Investment Solutions team partners with clients to create customised solutions that meet their unique needs for asset allocation, responsible investment beliefs, portfolio characteristics requirements, exclusions, legal wrapper, risk appetite and more.

We anticipate that returns across major asset classes will converge over the next five years. As a long-term investor, this presents you with an opportunity to reassess and refine your strategic asset allocation. Our experts share detailed forecasts and actionable recommendations.