In summary

Supporting documents

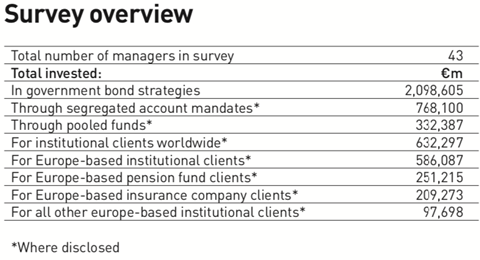

Click link to download and view these filesIPE survey - Managers of government bonds 2019

PDF, Size 0.56 mb

Many investors entered 2026 expecting slower growth, cooling inflation, and eventual Federal Reserve rate cuts. Instead, markets have faced a more complicated reality, with geopolitical tensions rising, oil prices moving higher, rates backing up, and investors pricing a meaningful probability of additional Fed tightening. Yet the U.S. economy remains resilient, inflation has generally improved, and productivity gains driven by technology and AI continue to support growth.

“As the Fed moves to reduce policy guidance, uncertainty over the short-rate path is likely to rise, creating additional volatility along the yield curve”

European private loans should not be read as simply another form of private credit. They are better understood as, on average, high-quality investment grade bank lending, with embedded illiquidity premia well suited for a tight spread environment.

Copyright © 1997–2026 IPE International Publishers Limited, Registered in England, Reg No. 3233596, VAT No. 685 1784 92. Registered Office: 1 Kentish Buildings, 125 Borough High Street, London SE1 1NP

Site powered by Webvision Cloud