In summary

Supporting documents

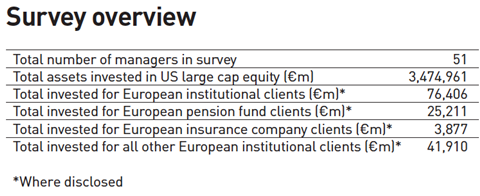

Click link to download and view these filesIPE Survey - US large cap equity managers 2019

PDF, Size 0.4 mb

Opportunities to speak before Congress are rare. So, when US lawmakers invited Capital Group Vice Chair Jody Jonsson to share her perspective on aligning public policy with shifting market conditions, she welcomed the chance.

“As the Fed moves to reduce policy guidance, uncertainty over the short-rate path is likely to rise, creating additional volatility along the yield curve”

Britain is one of the world’s great originators of ideas, yet too many of its most promising companies have had to look abroad for the capital to grow. Institutional investors have a rare chance to fund the next stage of that growth story and capture compelling long-run return streams.

Copyright © 1997–2026 IPE International Publishers Limited, Registered in England, Reg No. 3233596, VAT No. 685 1784 92. Registered Office: 1 Kentish Buildings, 125 Borough High Street, London SE1 1NP

Site powered by Webvision Cloud