In summary

Supporting documents

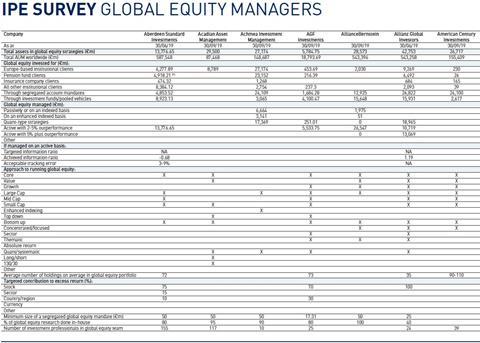

Click link to download and view these filesIPE Survey - Global equity managers 2019

PDF, Size 0.14 mb

Many investors entered 2026 expecting slower growth, cooling inflation, and eventual Federal Reserve rate cuts. Instead, markets have faced a more complicated reality, with geopolitical tensions rising, oil prices moving higher, rates backing up, and investors pricing a meaningful probability of additional Fed tightening. Yet the U.S. economy remains resilient, inflation has generally improved, and productivity gains driven by technology and AI continue to support growth.

The reform plus fiscal package is genuinely large and potentially a regime change, but not yet an unqualified “buy Germany/Europe” signal. The principal upside risk is a confidence-led private capex cycle. The key downside risk is implementation failures and higher bond yields, which could turn a productive investment programme into a less equity-friendly fiscal expansion.

Although the German economy is still characterised by a weak recovery, sluggish productivity and persistent supply constraints, the combination of an extensive infrastructure and defence spending programme and a package of 34 structural reforms is improving the medium-term outlook. While the direct impact on growth in 2027 is likely to be limited, more significant gains are expected over time, provided the reforms are implemented effectively.

Copyright © 1997–2026 IPE International Publishers Limited, Registered in England, Reg No. 3233596, VAT No. 685 1784 92. Registered Office: 1 Kentish Buildings, 125 Borough High Street, London SE1 1NP

Site powered by Webvision Cloud