Corporate Overview

Charter Hall (ASX:CHC) is Australia’s leading fully integrated diversified property investment and funds management group. We use our expertise to access, deploy, manage and invest equity to create value and generate superior returns for our investor customers. We’ve curated a diverse portfolio of high-quality properties across our core sectors – Office, Industrial & Logistics, Retail and Social Infrastructure.

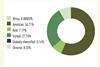

Operating with prudence, we have carefully curated an A$90.3 billion portfolio, comprising A$71.7 billion of property funds under management with over 1,600 high-quality, long-leased properties to more than 2,700 unique tenants.

Partnership and financial discipline are at the heart of our approach. Underpinning our focus on mutual success, our balance sheet capital is primarily invested alongside our investors, with more than A$2.8 billion co-invested in our funds and partnerships.

We take a long-term view, combining insight and inventiveness to unlock hidden value for our customers and communities. Our A$17.9 billion pipeline of develop-to-core projects delivers sustainable, technologically enabled, future-proofed assets that attract key customers and high-quality, long-term leases, ultimately delivering superior returns for our funds and partnerships.

The impacts of what we do are far-reaching. From helping businesses succeed by supporting their evolving workplace needs, to providing investors with superior returns, we support our customers, people and communities to grow.

Strategic corporate development

Charter Hall actively seeks out opportunities to strategically grow its business across Australia, with a strong emphasis on diversification through new funds, capital partners, tenant customers, asset acquisitions and our develop-to-core pipeline across all property sectors.

Through diversification of capital sources, we have built resilience into our business model, supported by a high-quality team focused on delivering outstanding results. Our strategic focus remains on investment funds and partnerships characterised by long WALE, high occupancy, and annual rent reviews, which deliver real income growth to our investors. Our development pipeline enables us to add value to existing assets while developing new high-quality, sustainable assets within our funds and partnerships.

Sector forecasts

INDUSTRIAL & LOGISTICS:

Overall conditions across the I&L market remain well balanced and constructive to further rental growth. Strong economic momentum and retail spending continue to support demand, while ongoing construction challenges continue to restrict the development of new I&L supply. Structural drivers remain with strong population growth, historically high levels of infrastructure development, growing e-commerce, and increased automation across logistics networks.

Tenant demand remains robust with 3.8 million sqm of leasing activity in the 12 months to Mar-26, 17% above the 10-year rolling average. Whilst supply is expected to fall further during CY26 with 2.5 million of new stock anticipated, representing a 27% fall compared to peak levels of supply in CY24. Vacancy remains some of the lowest levels globally, at 3.2% nationally.

Rents are forecast to continue to be driven by persistently low vacancy and the diminishing supply pipeline, with national face rents expected to grow at a more sustainable average rate of ~4.0% per annum over the next five years.

OFFICE:

Strong momentum continues across the Office markets, with the growth in leasing demand during CY25 reaching the highest level in five years. This has been driven by the growth in prime CBD leased stock, reaching 313,000 sqm, the highest level since Mar-19 and 47% above the 10-year average. Tenant demand remains concentrated in modern, high-quality buildings, with lower vacancy and stronger rental growth in these assets.

Restrictive construction conditions continue to limit new development, with new building completions trending down since the peak in Dec-2022. An upswing in tenant demand and downward trend in supply has generated notable rental growth. For national CBD markets prime net effective rental growth increased 7.4% per annum, the highest level since Sep-2018.

Forward-looking indicators highlight ongoing value recovery, with capital values up 6.6% y/y to Mar-26. Transaction volumes during 4Q25 were the highest level since Sep-2022 totalling $4.5 billion, with both domestic and offshore investors active in the market. The outlook is for further gradual improvement as supply remains limited and tenant demand strengthens, especially for modern, well-located assets.

RESIDENTIAL/ LIVING SECTOR:

High construction and financing costs, labour shortages, and a restrictive planning system are contributing to an undersupply of new housing. Current forecasts anticipate the National Housing Accord target of 1.2 million new homes will be missed by one third or more.

The apartment sector will be increasingly critical to support a ramp up in housing supply. However, the recovery of higher-density housing will take longer due to the lag between approvals and completions.

RETAIL:

The Retail sector continues to benefit from a cyclical upswing, evidenced by increased investor demand and sector-leading returns. Transaction activity reached $13.3 billion over the year to Mar-26, the highest volumes of the core real estate sectors and surpassing the long-term average by ~60%. The Retail sector has also generated the highest returns since mid-2022, with total returns of Retail Specialist funds growing +10.6% to Mar-26.

The rise in construction costs continues to have a profound impact on new development. Construction activity across the retail sector remains at historical lows, with CY25 supply the lowest level in the last 30 years. Strong ongoing population growth particularly in high-quality catchments where new retail supply is constrained, will continue to drive performance of retail assets in these areas.

Convenience-based retail assets which are characterised by a greater exposure to non-discretionary retailing (daily essentials such as groceries, medical, hardware and household goods) will continue to outperform larger, discretionary-focused shopping centres.

OTHER: Assets, such as childcare centres, senior housing, student accommodation, government premises and medical/health facilities, are becoming an increasingly attractive sector for investors. Essential by nature, these sectors continue to benefit from strong demand fundamentals.

Investment principles & strategy

Charter Hall is a fully integrated property investment management platform with expertise across investment management, property and asset management, transaction, leasing and development.

We are a leading owner and manager of long WALE assets that are predominantly leased to corporate and government tenants on long-term leases. Our focus on quality, well-located assets, with strong sustainability credentials and long-term leases, together with our ability to unlock hidden value, creates a balance between stability, returns and growth.

Our development pipeline enables us to add value to existing assets while creating new product within our funds to limit the need for buying assets in a competitive on-market environment.

Our extensive market presence enables us to provide cross-sector solutions to tenant customers. More than 69% of our tenant customers lease multiple tenancies from us, reflecting the value they find in our offerings.

Our leading market share in transactions, combined with our dedicated teams in each major metropolitan market, provides invaluable insight into local property markets. Over the past five years, we have undertaken A$42.8 billion in gross transactions, driven by the collaborative efforts of our investment management, transaction, property services and support teams, who together curate our portfolios for the benefit of our funds and partnerships.

A key competitive advantage is our unparalleled access to off-market deals, completing approximately 50% of all transactions in the last 5 years off-market. We also leverage our skills and relationships to partner with major corporate and government entities on sale and leaseback transactions. We have undertaken more than A$11bn in sale and leaseback transactions in the past 10 years, securing our position as the leader in the long WALE triple net lease sector.

Strategic corporate development

Charter Hall actively seeks out opportunities to strategically grow its business across Australia, with a strong emphasis on diversification through new funds, capital partners, tenant customers, asset acquisitions and our develop-to-core pipeline across all property sectors.

Through diversification of capital sources, we have built resilience into our business model, supported by a high-quality team focused on delivering outstanding results. Our strategic focus remains on investment funds and partnerships characterised by long WALE, high occupancy, and annual rent reviews, which deliver real income growth to our investors. Our development pipeline enables us to add value to existing assets while developing new high-quality, sustainable assets within our funds and partnerships.

Performance verification

As at 31 December 2025, CPOF outperformed the MSCI Core Office Index over the 10-year period. Over 10-year timeframe, CPOF has returned 5.4% p.a. in comparison to the MSCI Core Office Index 5.1% p.a.

As at 31 December 2025, CPIF continues to outperform the 10-year MSCI Core Index benchmark returns by 5.2%, post all fees (CPIF MSCI 10-Year Return 9.8% vs MSCI Core Index of 4.6%).

As at 31 December 2025, CCRF has returned 9.1% over 10 years and outperformed the MSCI benchmark by 6.3% as of 31 December 2025.

Compliance statement:

This information has been prepared by Charter Hall Funds Management Limited (ACN 082 991 786) (together, with its related bodies corporate, the Charter Hall Group). This information has been prepared without reference to your particular investment objectives, financial situation or needs and does not purport to contain all the information that a prospective investor may require in evaluating a possible investment. Prospective investors should conduct their own independent review, investigations and analysis of the information contained in or referred to in this publication and the further due diligence information provided. It is not an offer of securities or advice. Any forecast or other forward-looking statement contained in this information may involve significant elements of subjective judgement and assumptions as to future events which may or may not be correct. There are usually differences between forecast and actual results because events and actual circumstances frequently do not occur as forecast and these differences may be material. Charter Hall Group is not responsible for providing updated information to any prospective investors.

Note: Figures as of 31 December 2025 unless otherwise stated.