![CBRE Investment Management [Real Estate - Asia]](https://dvn7slupl96vm.cloudfront.net/Pictures/100x67fitpad[255]-90/P/web/t/j/u/cbreimlogohorizoutlcleanedup01green_654324.jpg)

Corporate overview

CBRE Investment Management is a leading global real assets investment management firm with $155.3 billion in assets under management* as of June 30, 2025, operating in 20 countries around the world. Through its investor-operator culture, the firm seeks to deliver sustainable investment solutions across real assets categories, geographies, risk profiles and execution formats so that its clients, people and communities thrive.

*Assets under management (AUM) refers to the fair market value of real assets-related investments with respect to which CBRE Investment Management provides, on a global basis, oversight, investment management services and other advice and which generally consist of investments in real assets; equity in funds and joint ventures; securities portfolios; operating companies and real assets-related loans. This AUM is intended principally to reflect the extent of CBRE Investment Management’s presence in the global real assets market, and its calculation of AUM may differ from the calculations of other asset managers and from its calculation of regulatory assets under management for purposes of certain regulatory filings.

Investment principles & strategy

CBRE Investment Management’s (the “Firm’s”) investment philosophy is to deliver superior performance by applying the Firm’s knowledge advantage through a disciplined investment process. The Firm’s investment philosophy is founded on the following principles:

Risk must be understood before it can be managed

- A rigorous risk framework for each mandate is formulated and then portfolios that will meet the firm’s clients’ risk/return requirements are carefully constructed.

Market conditions change

- By combining a global view of capital markets with an in-depth insight into local asset fundamentals, the firm invests in the markets and strategies that offer the best relative value at different stages of the cycle.

Every asset is unique

- The Firm utilizes its local information networks to understand the drivers and risks of the future cash flow of an asset, enabling the ability to see opportunities where others do not, and to be a disciplined seller.

Asset management creates value

- A deeper understanding of occupier requirements enables the Firm to maximize each asset’s potential through innovative and sustainable management.

Consistency counts over the long run

- A superior investment track record is built through consistent outperformance across cycles.

The Firm offers a range of strategies across the risk-return spectrum.

Sector forecasts

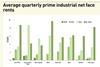

INDUSTRIAL: The logistics sector remains a cornerstone of Asia Pacific real estate, supported by structural drivers such as e-commerce growth, urbanization, and sustainability requirements. Demand for modern logistics facilities continues to outpace supply in key markets, including Japan, Australia, South Korea, and Singapore. Rent growth is expected to remain positive across most markets, with Australia forecast to deliver the strongest performance, albeit at a more moderate pace compared to recent years as vacancy normalizes from historic lows. Japan and South Korea are also projected to see above-average rent growth due to constrained supply pipelines and elevated construction costs. In contrast, China faces a weaker outlook, with negative rent growth in the near term due to elevated vacancy, though conditions are expected to improve later in the forecast period. Cap rate compression is anticipated in Australia and South Korea as monetary easing supports liquidity, while Japan’s logistics yields are expected to remain relatively stable before modest compression in the outer years. Overall, logistics is positioned to deliver strong total returns, particularly in markets where entry pricing remains attractive and occupier demand is resilient.

OFFICE: The office sector in Asia Pacific is entering a phase of selective recovery, with performance varying significantly by market and asset quality. Australia is forecast to deliver the strongest office rent growth over the next five years, driven by declining vacancy and a gradual return-to-office trend. South Korea also offers a favorable outlook, though new supply pipelines may temper growth. Japan’s office market is improving, supported by stable demand and limited new supply in core submarkets. However, bifurcation remains a defining theme: modern, ESG-compliant assets in prime locations are expected to outperform, while secondary offices face structural challenges and high repositioning costs. Cap rate compression is anticipated in Australia and South Korea, while Japan’s office yields are expected to remain relatively stable before modest tightening in later years.

RESIDENTIAL: Residential real estate continues to demonstrate resilience across Asia Pacific, underpinned by structural demand drivers such as urban migration, affordability challenges in homeownership, and demographic shifts. Japan’s residential market is forecast to achieve rent growth of 2.1% per annum over the next five years, outpacing domestic inflation expectations. Australia’s residential sector, including build-to-rent (BTR) and purpose-built student accommodation (PBSA), is expected to deliver even stronger rent growth at 3.3% per annum, supported by low vacancy and robust demand from international students. Liquidity in the sector remains healthy, and leverage is accretive in markets like Japan, where financing costs remain low and yield spreads are wide. Investors should prioritize assets in gateway cities with strong connectivity and sustainability credentials, as these factors increasingly influence occupier preferences and long-term value.

RETAIL: Retail is regaining investor attention in Asia Pacific, particularly in markets such as Australia, Singapore, and Japan. Shopping centers anchored by non-discretionary retail are well-positioned to deliver resilient income as consumer spending recovers. Australia’s retail sector benefits from improving economic conditions and strong household consumption, while Singapore’s defensive retail formats continue to attract capital due to their stability and integration with mixed-use developments. Although discretionary retail remains under pressure in some markets, necessity-driven formats and well-located assets with strong tenant covenants offer compelling opportunities. Yield compression prospects are strongest in markets where pricing has already rebased and fundamentals are improving, making retail a tactical allocation opportunity in diversified portfolios.

Strategic corporate development

CBRE Investment Management seeks to be a leader in global real assets investment management by consistently delivering outstanding performance and exceptional client solutions. The Firm continues to bolster its existing global platform and grow purposefully over time.

In particular, the Firm is focused on growing the following programs over the next three to five years in alignment with investor appetite and objectives:

- Open-end, diversified core real estate funds in the U.S. and Europe

- Open-end, diversified global core-plus funds in real estate and infrastructure

- Open-end, sector-specific core-plus funds in logistics and residential in the U.S. and Europe

- Closed-end, enhanced return real estate fund series in the U.S., Europe, and APAC, plus a global opportunistic secondaries fund series

- Listed real assets strategies across real estate and infrastructure

- A select number of premier separate accounts across asset classes, regions, and/or execution formats.

CBRE Investment Management does not place absolute limits on growth in any of the above areas, with the exception of selective hard ceilings on closed-end funds based on overall capacity of the investment opportunity. In general, the Firm would limit growth if the expected high level of performance or service could not be provided or when growth would jeopardize the performance of existing investments.

We do not foresee any potential conflict of interest that could arise from managing this particular account.

COMPLIANCE STATEMENT

Senior management of CBRE Investment Management is responsible for ensuring compliance with a code of ethics, regulatory requirements, and fiduciary obligations.

CBRE Investment Management is an investment adviser registered with the Securities and Exchange Commission under the Investment Advisers Act of 1940. It also is authorized and regulated in certain European and Asian countries to undertake certain regulated activities in conjunction with its investment advisory and fund management services.

The firm has designated compliance officers across the regions and has adopted, implemented, and provided for reviews of adequacy and effectiveness of its written policies and procedures.

All employees are required to comply with the Investment Management Policies and Procedures, which include legal and compliance policies.

This information is for informational purposes only. Past performance is not indicative of future results, and the value of investments can go down as well as up. Investing involves risk, including the loss of your entire investment.

![CBRE Investment Management [Real Estate - Asia]](https://dvn7slupl96vm.cloudfront.net/Pictures/100x67fitpad[255]-90/P/Pictures/web/t/j/u/cbreimlogohorizoutlcleanedup01green_654324.jpg)