Fixed Income – Page 20

-

White papers

White papersEuropean Private Loans Benefit from Credit Crunch

With Europe’s public debt markets tightening as its corporate borrowers seek to refinance, private lenders sense an opportunity.

-

White papers

White papersWhat’s in Store for US Insurers in 2023?

Insurers’ risk controls and investment skills faced stiff tests in 2022, as both inflation and interest rates skyrocketed and nearly every asset class endured a sharp selloff. With traditional diversification approaches failing, investors had nowhere to hide.

-

White papers

White papers10 investment themes for 2023

Although many investors are expecting a return to normal after inflation subsides and central banks stop raising interest rates, we believe markets are undergoing significant changes and it might be necessary to reset expectations in this new environment.

-

White papers

White papersClimate Transition: Burning Questions for Credit Strategies

Transitioning the global economy to net-zero emissions presents a significant challenge, but it also offers an opportunity for fixed income investors—in energy, utilities, and beyond.

-

White papers

White papersIs 2023 the year of value-add?

These are, it has to be said, dramatic times. No sooner than most of the world was starting to emerge from the long shadow of the COVID-19 pandemic, it was confronted with another crisis.

-

White papers

White papersActive fixed income ETFs in the spotlight

Given challenging market conditions, it looks like the time for active fixed income ETFs to shine, according to Jason Xavier, Head of EMEA ETF Capital Markets. He explains why he sees more growth in this area.

-

White papers

White papersFixed Income: Securitized sectors outlook and opportunities

Fixed income is once again offering income, leading to attractive risk-adjusted return profiles in some segments of securitized sectors. As investors look to take advantage of higher yields, securitized sectors can offer not only income opportunities, but also uncorrelated returns and diversification benefits.

-

White papers

White papersNew data hints rate hiking is far from over

Plans for the European Central Bank (ECB) to continue to hike interest rates gain momentum following better-than-expected economic data releases.

-

White papers

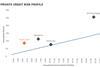

White papersHard to Ignore: Risk/Return Profiles of Private Credit and Senior Private Credit

The size of the private debt market currently stands at an estimated $1.2 trillion. And with private credit AUM increasing over 10% annually for the past decade, Hamilton Lane believes that the opportunity for future investment remains robust.

-

White papers

White papersNotes from the Road: Inflation, Private Assets and a Cautious Consensus

The beginning of the year always offers a chance to catch up with a broad range of clients who are in the mode of thinking about the big picture outlook: pension funds, insurers, consultants and sovereign wealth funds across Australia, Asia, Europe and North America. This note reflects on the key issues that clients have wanted to talk about in the early months of this year. Collectively, these topics give us a picture of what’s on investors’ minds.

-

White papers

White papersMulti-sector fixed income 2023

2022 was a year for the record books in U.S. fixed income markets. The Bloomberg U.S. Aggregate Bond Index (“the Agg”) celebrates its 50th anniversary in 2023. In those 50 years, 2022’s calendar year total return of -13.01% was unprecedented. The prior record was 1994 (-2.92%); in fact, the cumulative total return of the previous four negative years (1994, 1999, 2013, and 2021) was only -7.30%

-

White papers

White papersTime For A Fresh Look At Money Markets

There is good news for investors wishing to park their cash short term before deploying capital for the longer term. As central banks raise rates, so yields in money markets are rising, with the likelihood of further rises to come.

-

White papers

White papers360° fixed income report Q1 2023: Inflation, disinflation, inflection

In the latest edition of our 360° report, the team reflect on what has been a promising start for fixed income in 2023. Can the rally sustain, has too much of the good news already been priced in, and what will shape the narrative over the course of this year?

-

White papers

White papersPolitics, Deficits and the Debt Limit

We firmly believe that Congress will ultimately raise the debt limit, but it’s worth remembering that political drama affects markets.

-

White papers

White papersHigh yield bonds vs. leveraged bank loans: Is now the time to rotate?

Over the last two years, leveraged U.S. bank loans (“loans”) have outperformed their high yield bond counterparts; however, we believe this trend may be coming to an end. The relative outperformance of loans during this period was primarily a function of duration, or more notably in 2022, the lack of duration.

-

White papers

White papersClimate Transition Credit at Allspring

Investors can pursue both their climate objectives and financial goals through their bond allocations. In this blog post, we outline the opportunity in climate transition credit.

-

White papers

White papersNon-Investment Grade Defaults: Up From the Lows, but Contained

With defaults rising off of all-time lows, but likely remaining well below recession norms, we remain constructive on high yield and non-investment grade credit.

-

White papers

White papersWhy Does Private Credit Remain a Compelling Investment Opportunity vs High Yield Bonds in the Current Economic Environment?

As the U.S and Europe transition into a new era of tighter monetary policy, higher interest rates have had dramatic consequences across virtually all asset classes. Bonds were amongst the hardest hit given the interest rate risk inherent with any fixed payment security.

-

White papers

White papersGSS bonds: The sustainable bond market of cities and regions

The Franklin Templeton Fixed Income team believe investors with an appetite for sustainable impact should focus their attention on the market of urban GSS bonds.

-

White papers

White papersEmerging Markets Debt: will 2023’s bright start last the course?

Maybe it’s an optimistic time of the year or maybe it’s just a good investment case? Whatever you identify as the driver, there is no denying that 2023 has begun in extraordinary fashion for emerging markets debt (EMD).